Is Inflation Relief on the Horizon?

This year, inflation has been a problem for consumers as prices have risen on food, gas and a variety of other goods and services. Inflation refers to the overall increase in prices for goods and services in an economy. Inflation is significant for many reasons. One reason is that it causes higher prices. It is also the arch enemy of fixed investments like Mortgage Bonds because it erodes the buying power of a Bond’s fixed rate of return. Another impact of inflation is that it often leads to higher interest rates. This happens because when inflation is rising, investors demand a rate of return that is high enough to combat the faster pace of erosion. As a result, inflation can have a significant impact on the economy and on individuals’ financial well-being. But is there relief on the horizon?

The Feds Concerns

Inflation has been a concern for the Fed since late last year. In response, they have hiked their benchmark Fed Funds Rate five times so far this year. Their latest aggressive 75 basis point hike was at their meeting on September 21. The Fed Funds Rate is the interest rate for overnight borrowing for banks and it is not the same as mortgage rates. When the Fed hikes the Fed Funds Rate, they are trying to slow the economy and curb inflation. However, inflationary pressures have persisted despite the Fed’s efforts, and there is growing pressure on the central bank to take more aggressive action. While inflation remains a concern, it is important to remember that it is not the only factor influencing the Fed’s decision-making. They must also consider the health of the overall economy and financial markets when making policy decisions.

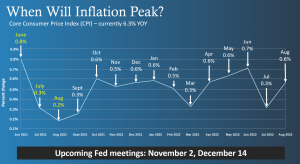

Inflationary Pressures

Inflation has been on the rise in recent months, but it’s important to remember that inflationary pressures are often cyclical. As the chart shows, inflation has historically risen and fallen in fairly predictable patterns. While it’s impossible to say exactly when inflation will start to decline, we can look at previous patterns to get a sense of when it might start to ease off. Based on the data, it appears that inflation may start to moderate in the next few months giving some relief. This would be welcome news for homebuyers, as it would likely lead to lower mortgage rates.

Understanding the CPI (Consumer Price Index)

In order to understand how inflation is calculated, it is first important to know what CPI is. CPI, or the Consumer Price Index, is a measure of the average change in prices paid by urban consumers for a market basket of consumer goods and services. The CPI market basket includes items such as food, housing, apparel, transportation, and medical care. The CPI is used to calculate inflation. Which is the percentage change in the CPI from one period to another.

In order to calculate the inflation rate, the Bureau of Labor Statistics takes the total of the past 12 monthly CPI readings and compares it to the total from the previous 12-month period. This 12-month rolling basis is how inflation is calculated. When the data for August 2022 of 0.6% was released on September 13, it replaced 0.2% from August 2021, causing annual Core CPI to rise from 5.9% in July to 6.3% in August. Investors can make more informed decisions about where to allocate their resources.

Recession Like Numbers

If we start to see more realistic recession-like numbers for inflation this fall, such as 0.1% or 0.2% a month from October onwards, these would replace the higher comparisons of 0.5% and 0.6% as seen in the chart. We could see the year-over-year rate of inflation decline by 2% by the time January's reading is released in February of next year. This would bring Core CPI down from 6.3% to just over 4% year over year and provide some relief.

Month over Month Inflation

The chart makes it easy to compare inflation rates from one month to the next. And to spot patterns over time. For example, the chart shows that inflation has been rising since February 2021. After a period of relatively low inflation in 2020. However, it seems likely that this upward trend will continue. With higher inflation rates in April, May and June of that year. The rate of inflation is likely to slow down. As the high numbers from 2022 are replaced by lower numbers in 2023. This illustrates how important it is to keep track of changes in the rate of inflation. In order to make informed decisions about personal finances, investment, and debt relief.

Bottom Line

However, some economists believe that inflation may start to slow in the coming months. If the Core CPI falls below 3%, it could have a positive impact on mortgage rates. Lower inflation could lead to lower mortgage rates. This would be welcome news for potential home buyers who have been struggling to afford a home. While it’s impossible to predict the future, the bottom line is that lower inflation could bring an improvement in mortgage rates next year. If you would like more information on the current market and what you can do to feel some relief click the button below to schedule an appointment with one of our experienced mortgage advisors.