Why You Need a Better Rate

You might not think that your mortgage rate matters, but it could help you save thousands over the life of your loan. Learn how to find and compare rates online today!

What is a mortgage rate and why does it matter?

Mortgage rates determine how much interest accrues on your home loan. The higher your rate, the more money you’ll end up paying for that house! In this context it’s important to know if a fixed-rate mortgage or adjustable rate one (ARM). Let me explain what they both entail.

Fixed-Rate: A fixed-rate mortgage means that the amount of your monthly payment that goes toward principal and interest stays pretty much constant for as long you have this loan. Although over time, if taken out correctly in an effort to save money on interest payments by locking down rates for 20 years or more, it becomes possible to pay less than before because there will always be so much devoted solely towards paying off what was borrowed – even though at least initially some extra cash would go straight back into making up lost funds rather than allowing them accumulate further through higher yields elsewhere (ie: increasing equity).

Adjustable Rates (ARMs): ARMs are a bit different. They typically start with an introductory rate that remains fixed for the first several years of your loan – usually around 5, 7 or 10 depending on how long you want to borrow and what kind of financing option best suits your needs in the meantime! Once this initial period is over though there will be periodic adjustments up or down according to market conditions which could mean savings each month if things go well while interest rates change often so it’s important not only know more about these loans before signing anything just yet.

What factors go into mortgage rates

Now that you understand the difference between fixed-rate and ARMs let’s get into the details of the factors that can affect your rates.

Baseline Market

To understand how mortgage rates are set, it helps to know a little bit about the mortgage market. When you get your loan from an investor, mortgages in bonds which can be traded on exchanges like any other security or stock with different levels of risk associated depending upon who is buying them and selling these MBSs off again just like they do stocks at times!

Mortgage loans have their own complex economic system that revolves around interest payments every ten years when borrowers come up for renewal but there isn’t always consistency here because each company handles things differently so ask away before committing yourself

A mortgage backed securities (MBS) is a safe investment because it’s assumed borrowers will always make their monthly payments. The rate of return, however, tends to be lower than most other types of investments such as stocks and bonds- meaning they’re not necessarily right for everyone!

If you want good returns with low risk then an MBS might be just what you’re looking for; but there are some drawbacks too: Like any type of financial product or service out on the market today – prices can change at any time based solely on supply & demand which makes them unpredictable . That being said if somebody has been making regular honorable debt repayments up until this point I wouldn’t say no when asked about investing my hard earned cash into

If people are feeling optimistic about the economic future of our country and world, they tend to put more money in stocks. This is risky but also offers a greater potential reward than with bonds or mortgage-backed securities (MBS). When things feel less hopeful for tomorrow’s economy–whether it be because we’re currently experiencing an unemployment rate high enough so that many individuals can no longer afford their debts; fearing another major global recession will hit soon after one already did recently ended 2009 without any signs yet suggesting improvement oncoming anytime soon

The higher the demand for mortgage-backed securities, or MBS in this case, the lower its yield needs to be. The fact that investors are willing and able to buy these bonds at ever decreasing rates means there’s less risk involved which attracts them even more so than with other investments where interest would not always fluctuate as wildly from month-to-month because yields stay fairly constant regardless of whether it is a bull market era like during dotcom days when high flyers were riding high or now post financial crisis dip.

Other factors that affect your rate:

- Property itself

- Type of loan

- Credit score

- Size of down payment

- You have control over your rate

- Lender

Finding the rate that works for you

To help find the best rate for you

Use our tool! Mortgage Calculator

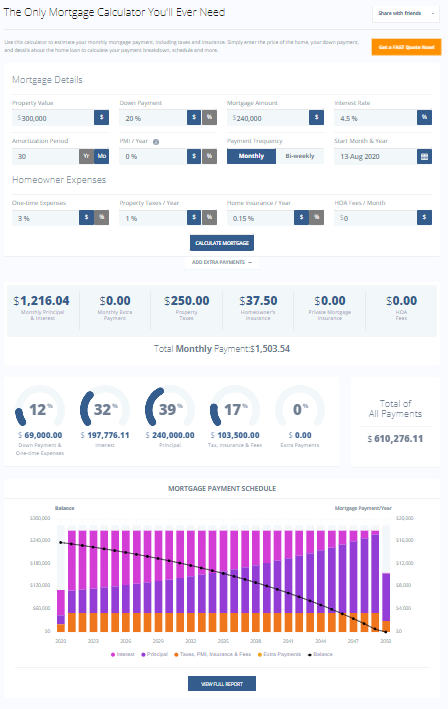

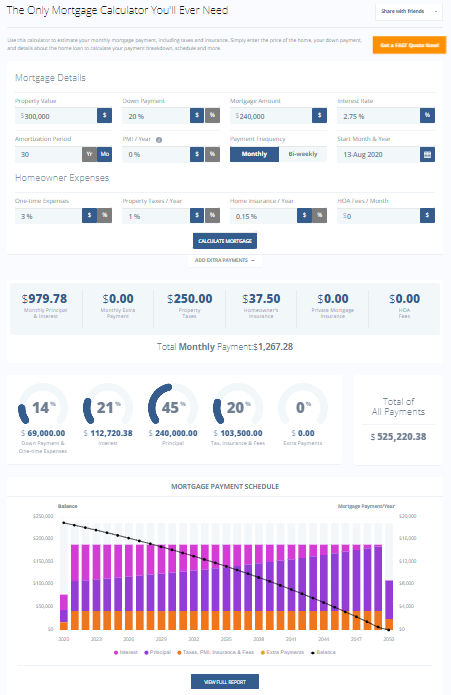

Example scenario:

4.5% vs. 2.75%

How to get better pricing

When it comes to mortgage rates, lower is better. Here are some things that can help you achieve better pricing.

Shorten Your Loan Term

Consider shortening your loan term. You can save a lot of money if you shorten your term from 30 to 15 years. Even if it's just 27, not only do I get lower interest rates but also pay off my mortgage sooner because investors don’t project inflation as far out in time!

Although your monthly payment would be higher, you're also likely to save tens of thousands in interest over the life of a loan. Not only will that mean less money for interest on each month’s installment as well as an easier time saving up those pennies- at least when compared with traditional 30 year loans!

Pay Off Debt

Closing certain accounts can be helpful in reducing debt. For example, paying off high-interest credit card debts is one way to free up more money for your monthly mortgage payment and reduce rates on other loans or lines of credit you have with lenders who offer better terms because they know how important this step may seem after doing some financial planning!

Paying down those pesky bills will allow us the opportunity take out a new loan at less cost as well as freeing ourselves from any negative marks on our report due solely by making such an effort towards settling these obligations quicker than expected – all while keeping things tidy within budgeting limits too.

Prepaid Interest Point

You can buy your rate down by prepaying interest at closing. This is done in the form of mortgage points, which are like coupons that come with every loan and offer discounts for paying early on them before their actual use date; each point equates to 1% off (or $1,000). You’re able to purchase these up until 0.125 per cent has been allocated towards this fee–so if you wanted only 75%, then 25 would go specifically toward getting those lower than average rates!

You can prepay interest to save money on your mortgage. The trade-off here is that you have to stay in the home long enough and pay off all of those pesky fees, but it will get you a lower rate than if we were just saving them up for later! If buying two points on a $250,000 loan (points cost around 5k) saved me thirty dollars each month by reducing my annual percentage rates from 4% down 2%, then I’d only need 17 months worth or residence before breaking even because at least one point has been paid off already.”

Higher Down Payment

A higher down payment at closing will get home buyers a lower rate. Putting down the majority of your purchase price lowers the relative risk for lenders, which means they are more likely to offer you an attractive interest rate and terms on any loans needed for this investment property or real estate development project!

The less equity shared with them (which can be seen through LTV), but also consider that amount these days if anything over 20%, then it becomes risky territory – meaning there could potentially come some strings attached just because their own liability goes up by about 30%.

Bottom Line

It’s important to get the best rate possible. A personal financial profile can help you win more competitive rates, and it will also show that you’re knowledgeable about your own situation when lenders are shopping for loans in order to get up-to date on any new legislation or updates with interest rates

It may seem daunting trying to find a good mortgage company but this article provides some helpful tips on how they compare apples-to-apples so there is no bias during negotiations!

Your Next Steps

If you're ready to take the next steps to lower your rate give one of our experienced mortgage advisors a call at (877)306-0222 or schedule a home financing consultation for a time that works best for you. Schedule a Home Financing Consultation.